2.0 KiB

2-Period RSI

This strategy was taken from chapter 9 of Short Term Trading Strategies That Work (2008) by Larry Connors.

Rules

The original long-only rules from the book:

- The asset (e.g., SPY) is above its 200-day moving average.

- The 2-period RSI closes below 5.

- Enter a long position at the close (or the following open in this case).

- Exit the position when the asset closes above its 5-period moving average.

For taking short positions, invert the above conditions and use a 2-period RSI reading of > 95 as the entry threshold.

Parameters

RSI Period: The period to use in the RSI calculation. (Default: 2)

RSI Smoothing: The smoothing period to use in the RSI calculation (Default: 1)

Long Entry Threshold: The RSI value below which to allow entering a long position. (Default: 5)

Short Entry Threshold: The RSI value above which to allow entering a short position. (Default: 95)

Long Term Trend Period: The period to use for the simple moving average used to define the long term trend. (Default: 200)

Short Term Trend Period: The period to use for the simple moving average used to define the short term trend. (Default: 5)

Use Fixed Position Sizing: Whether to use the same position size for every trade in order to neutralize the effect of lower historical prices. (Default: false)

Fixed Position Size: The size of the position when using fixed position sizing. (Default: 10000)

Long Only: Whether to only allow long trades as in the original strategy definition. (Default: false)

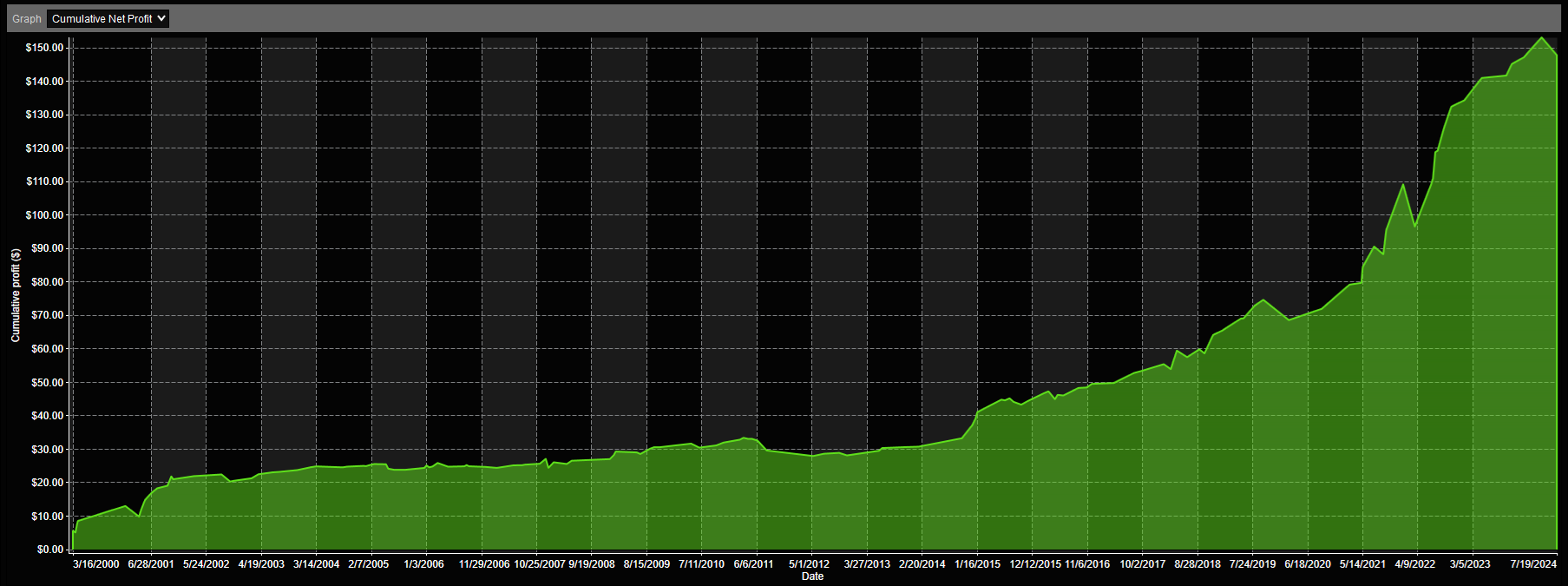

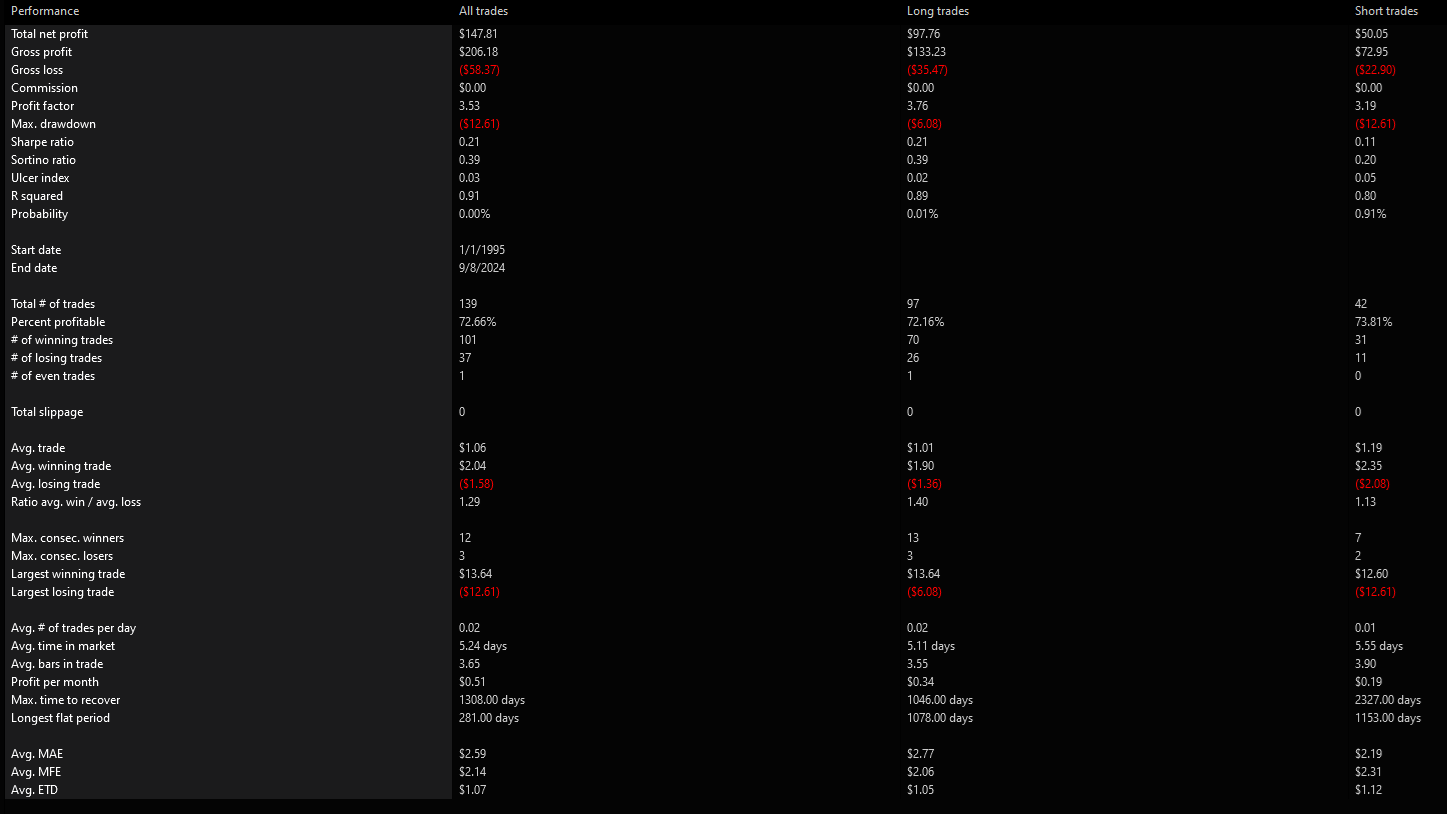

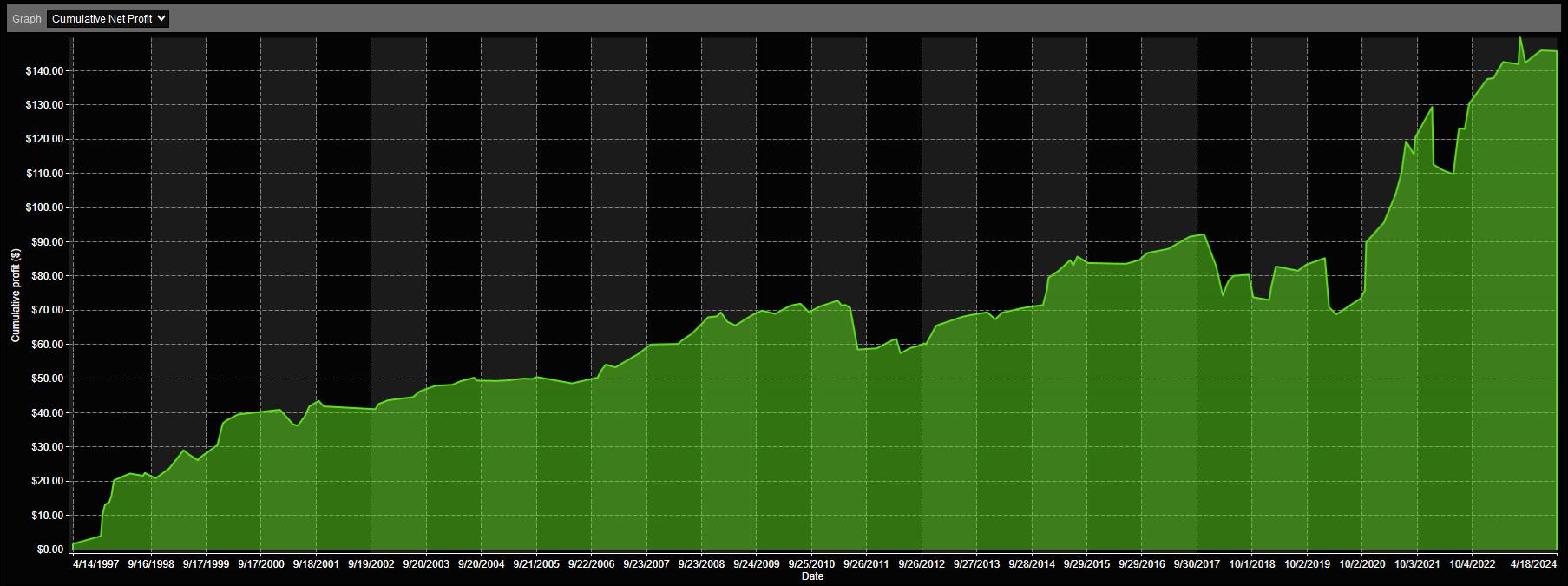

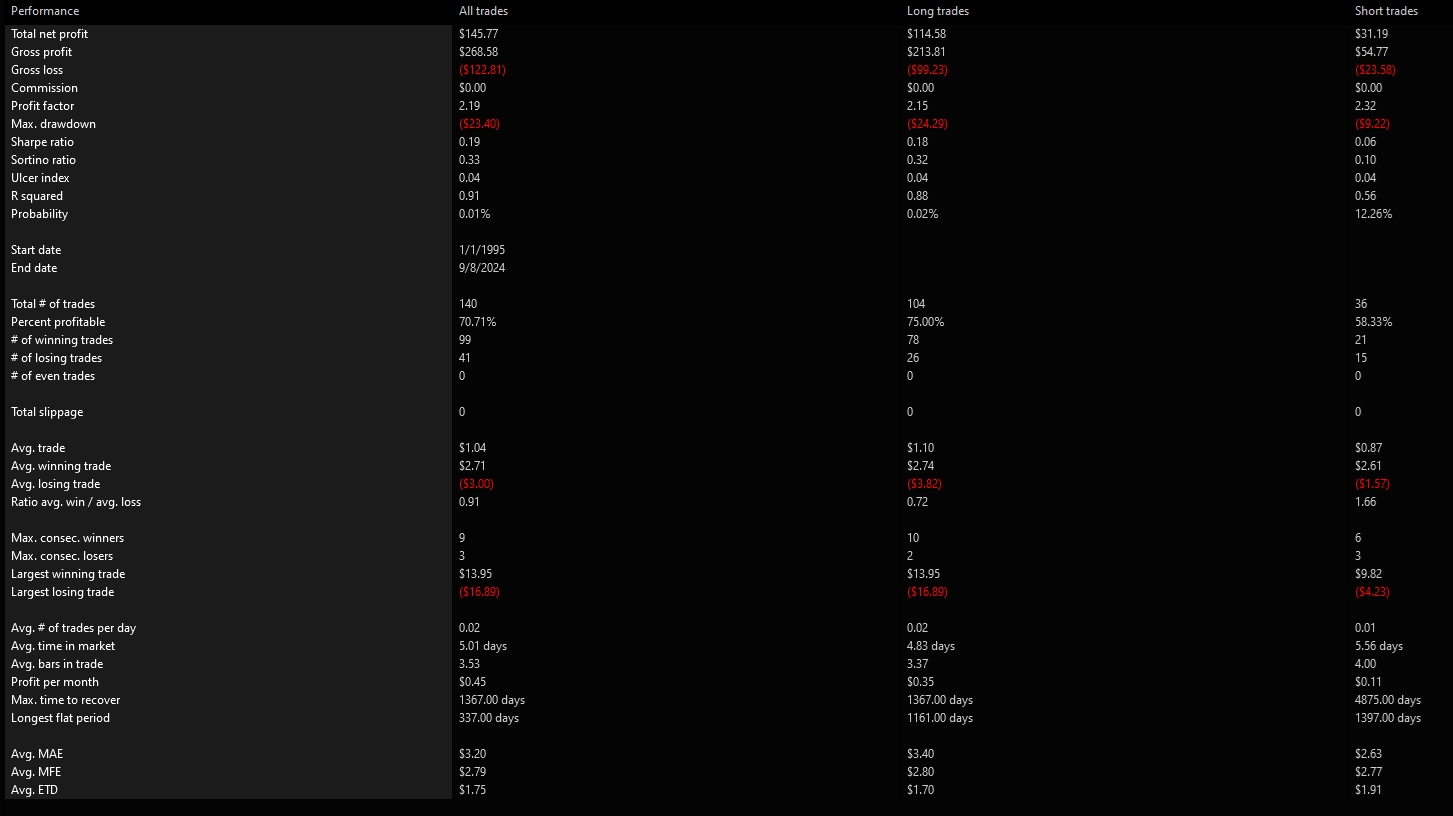

Backtest Results

SPY

QQQ