| .. | ||

| backtest-results | ||

| CumulativeRSIBot.cs | ||

| README.md | ||

Cumulative RSI

This strategy was taken from chapter 9 of Short Term Trading Strategies That Work (2008) by Larry Connors.

It is based on the Cumulative RSI indicator described in the book.

Rules

An alternate set of rules is provided in chapter 12 as follows:

- The asset (e.g., SPY) is above its 200-day moving average.

- If the 2-day cumulative 3-period RSI is below 45, enter a long position.

- Exit the position when the 2-period RSI is above 65.

Parameters

Cumulative RSI Period: The period to use in the RSI calculation. (Default: 2)

Cumulative RSI Smoothing: The smoothing to use in the RSI calculation. (Default: 1, no smoothing)

Cumulative Period: The number of RSI values to add up. (Default: 2)

RSI Period: The period of the RSI used to exit trades. (Default: 2)

RSI Smoothing: The smoothing of the RSI used to exit trades. (Default: 1)

SMA Period: The period used to calculate the long term trend as measured using a simple moving average. (Default: 200)

Entry Threshold: The Cumulative RSI threshold below which a trade is entered. (Default: 35)

Exit Threshold: The RSI threshold above which a trade is exited. (Default: 65)

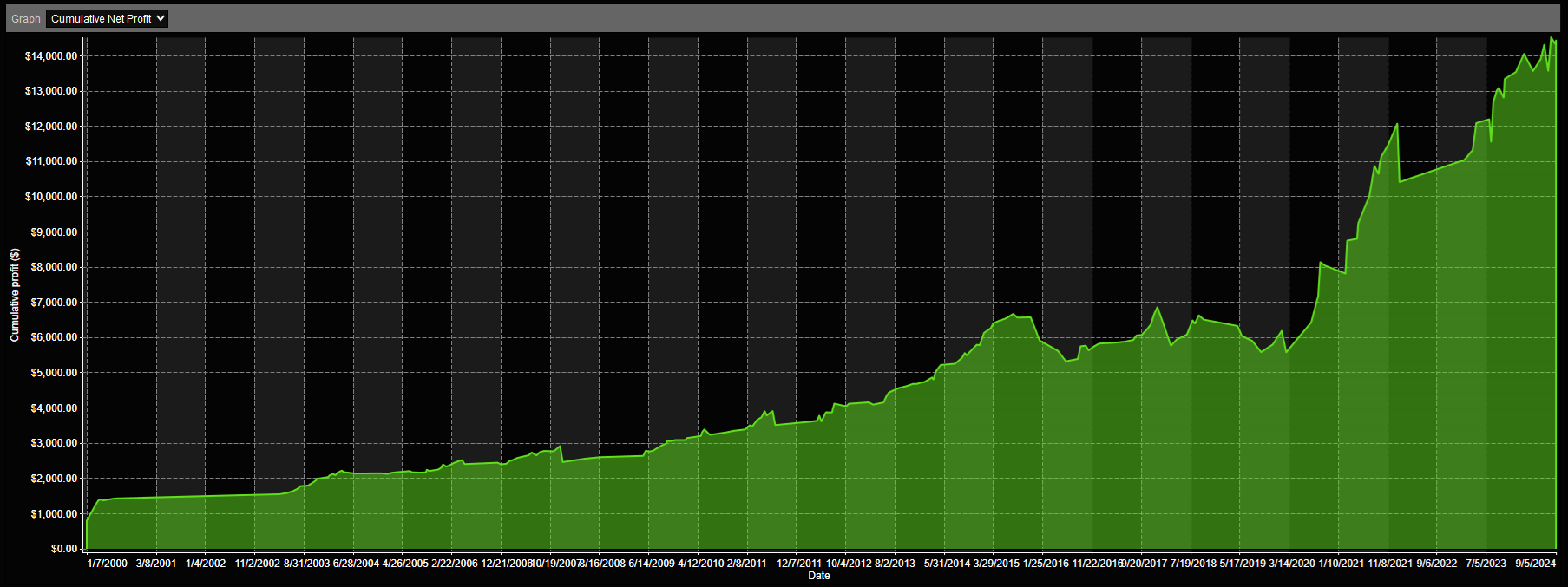

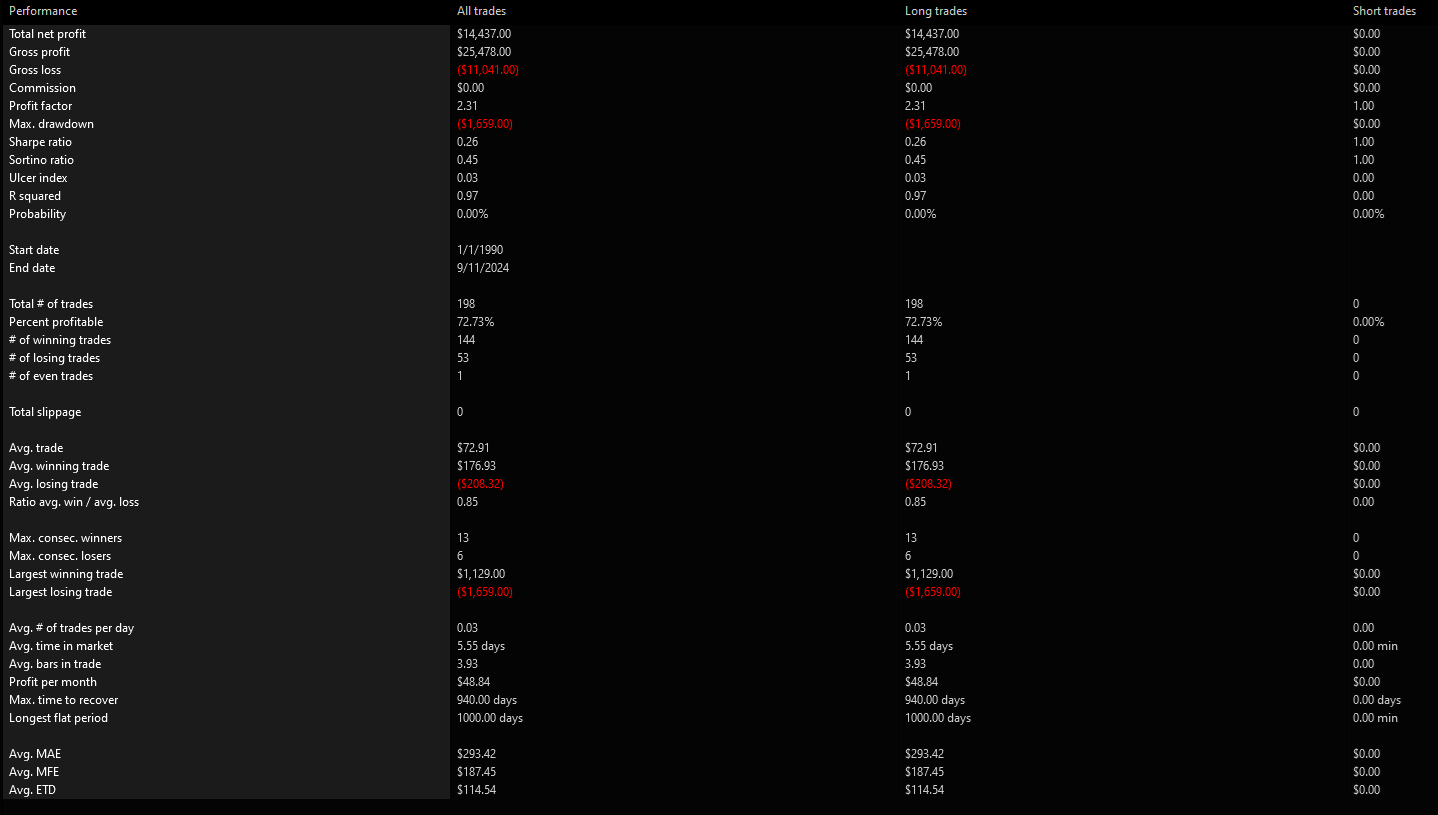

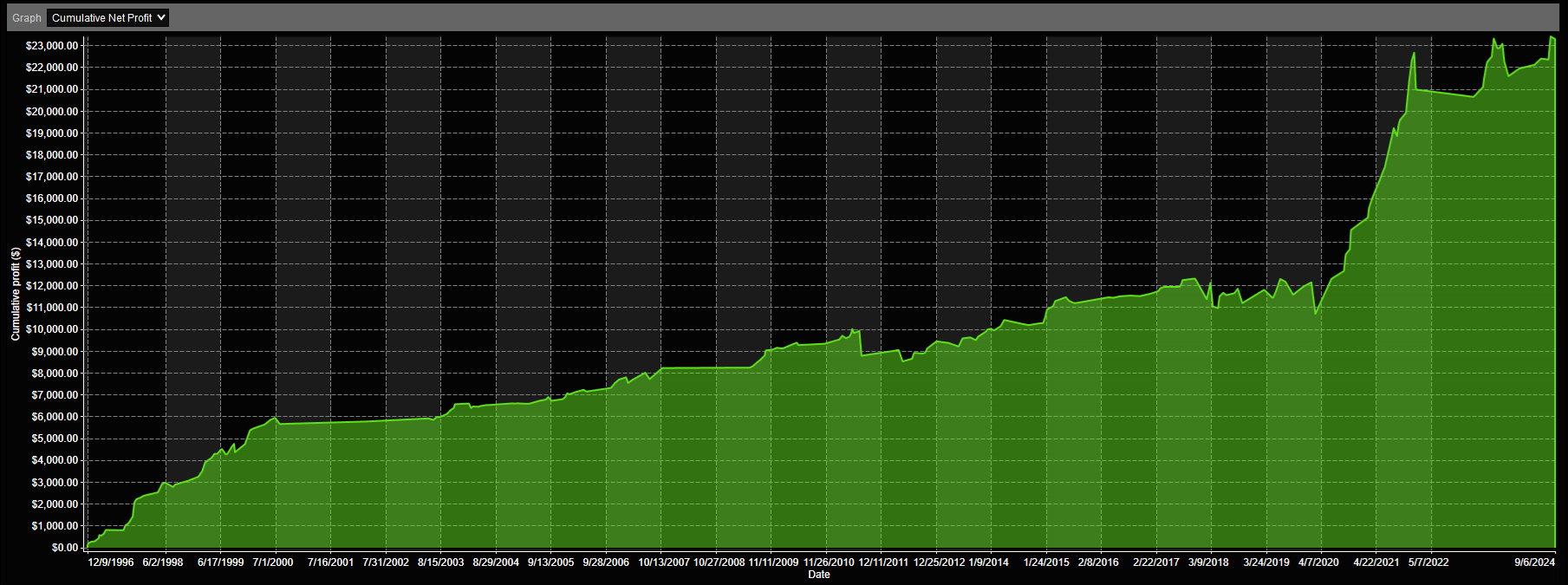

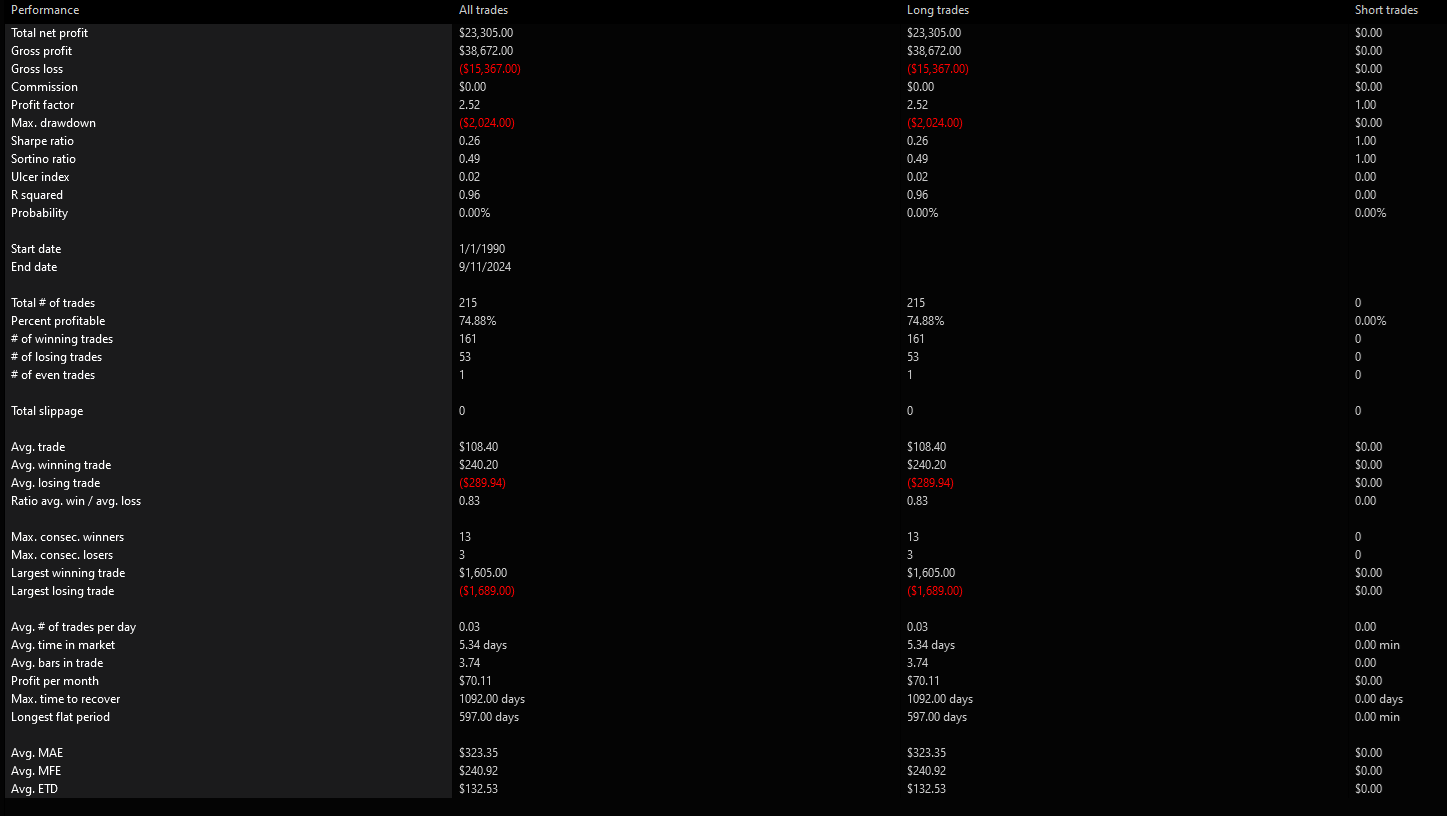

Backtest Results

SPY

QQQ