|

…

|

||

|---|---|---|

| .. | ||

| backtest-results | ||

| IBSRSI.cs | ||

| README.md | ||

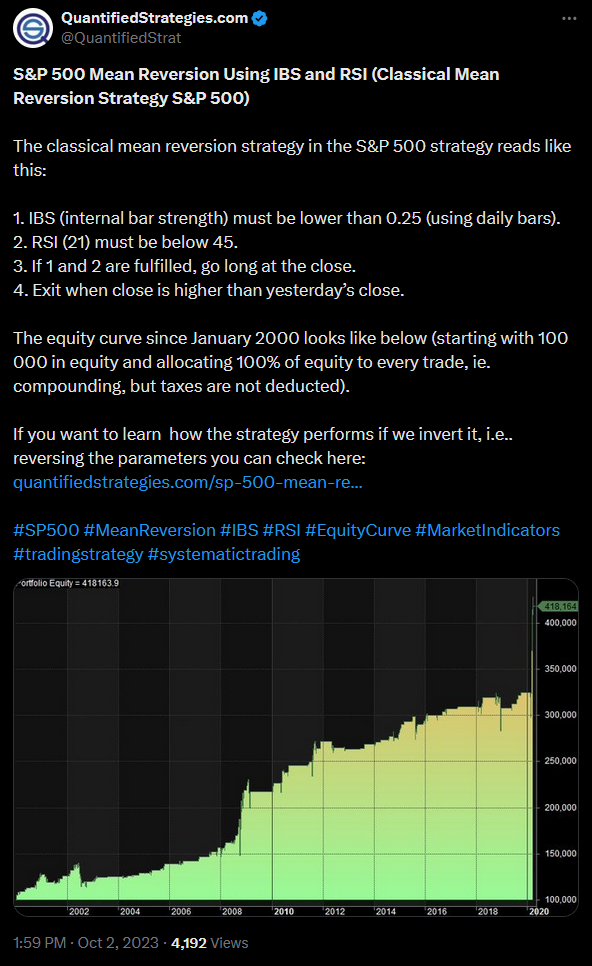

IBS + RSI

This is a mean reversion strategy based on the IBS (Internal Bar Strength) and RSI (Relative Strength Index) indicators.

The strategy was inspired by the following:

Rules

- The asset's (e.g., SPY) IBS must be < 0.25.

- If the 21-period RSI is < 45, enter a long trade.

- Exit the trade when the current day's close is higher than the previous day's close.

Parameters

RSI Period: The period used in the RSI calculation. (Default: 21)

IBS Threshold: The IBS value below which a long trade can be entered. (Default: 0.25)

RSI Threshold: The RSI value below which a long trade can be entered. (Default: 45.0)

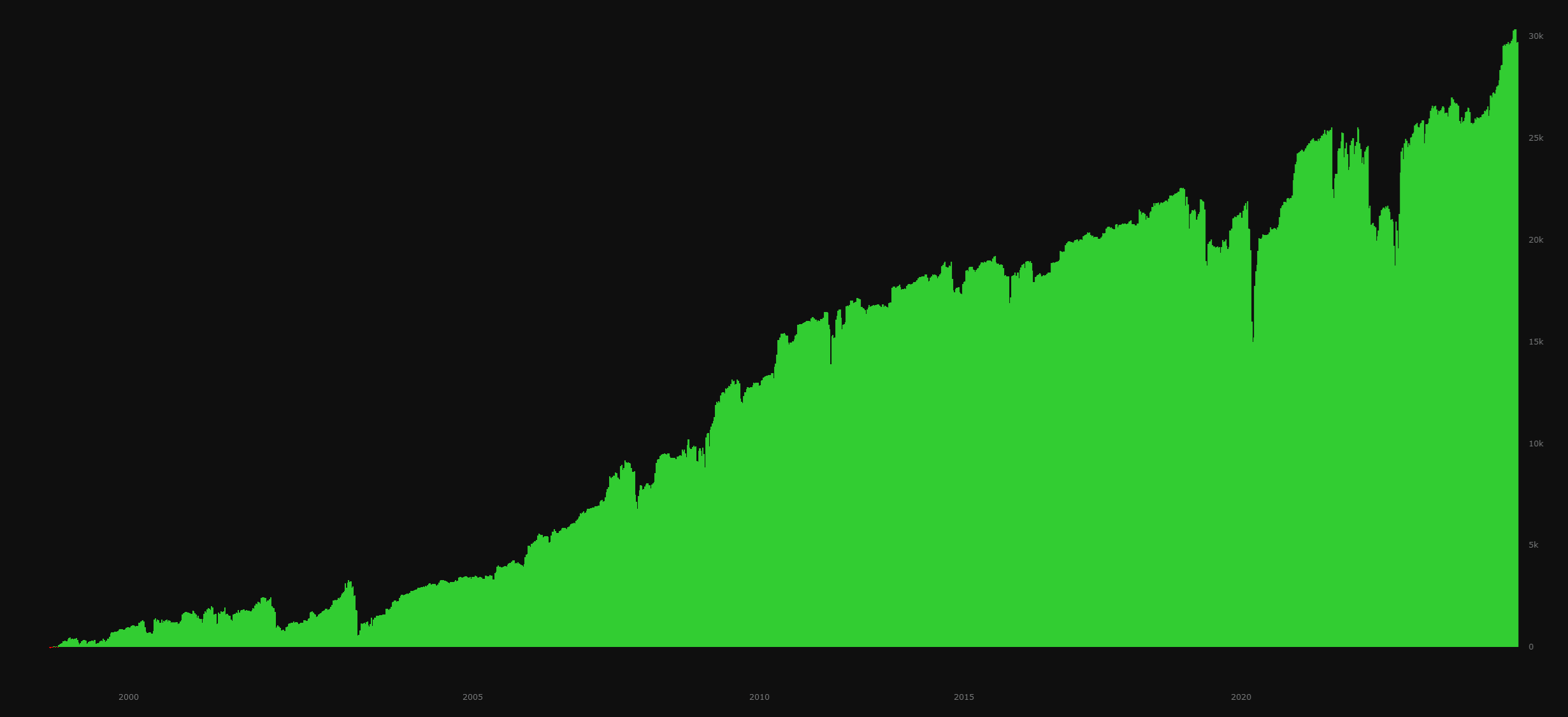

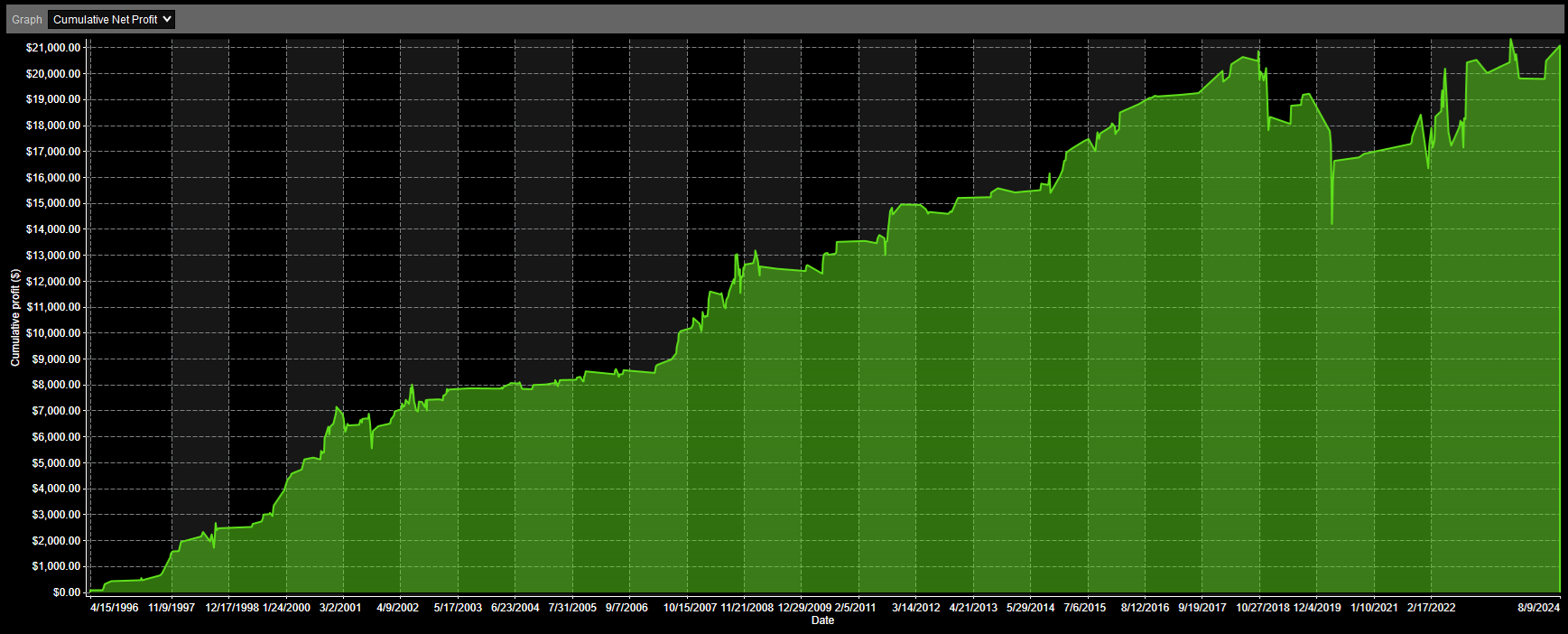

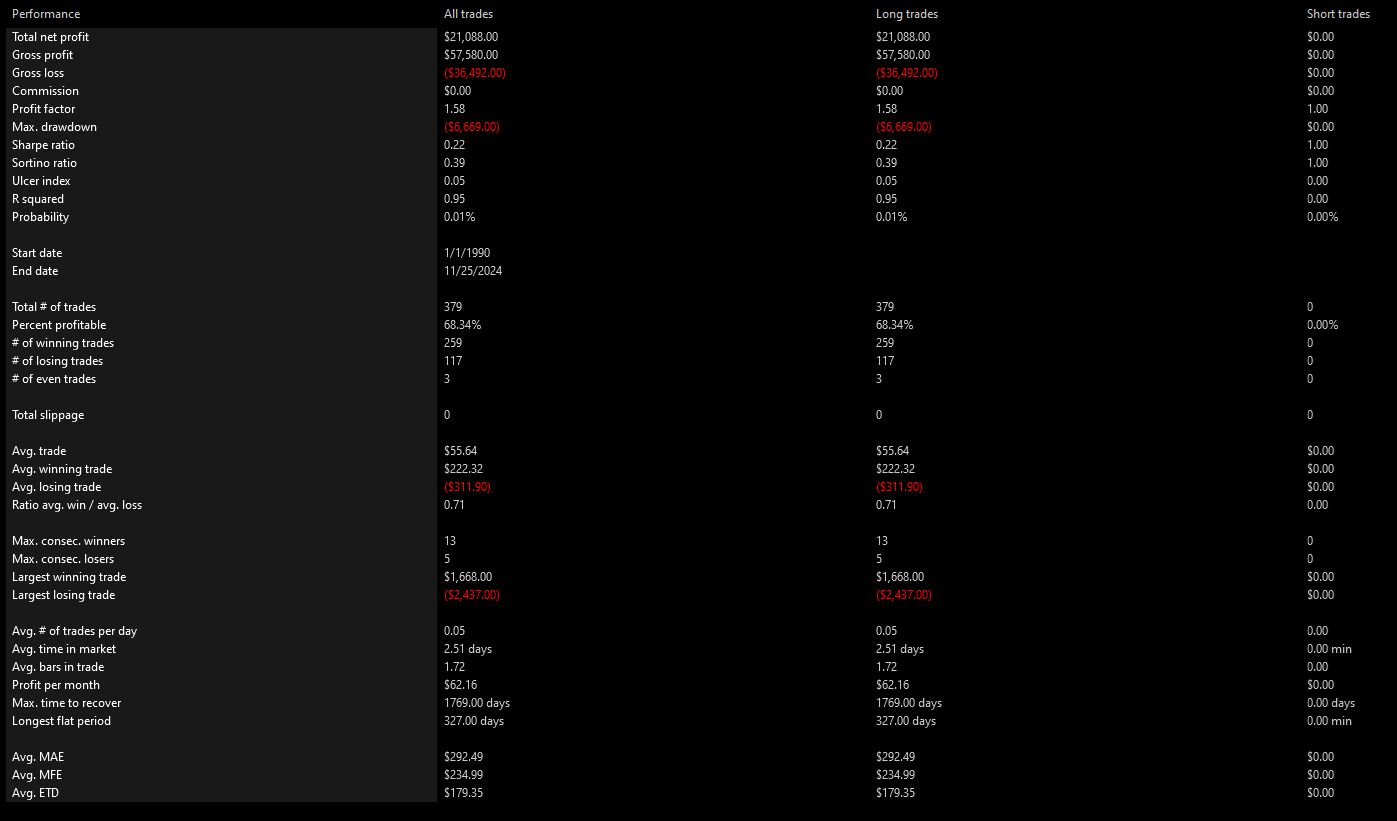

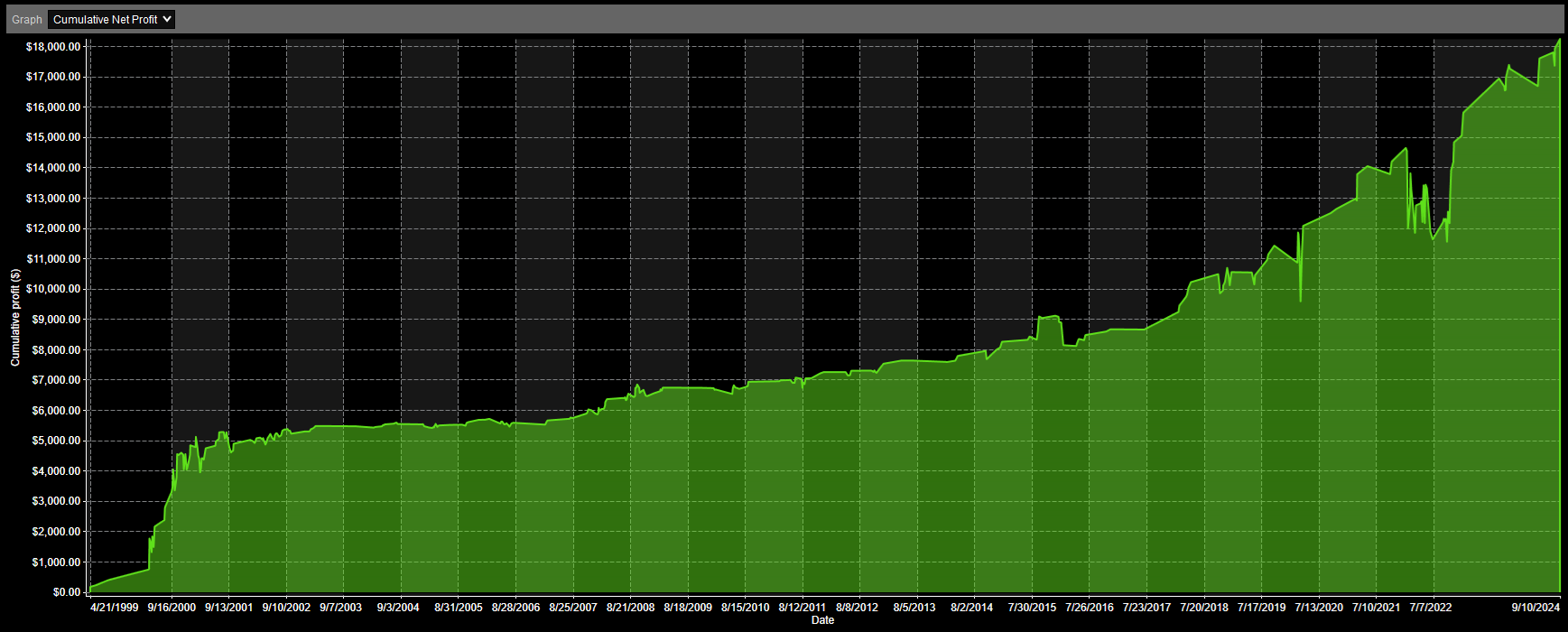

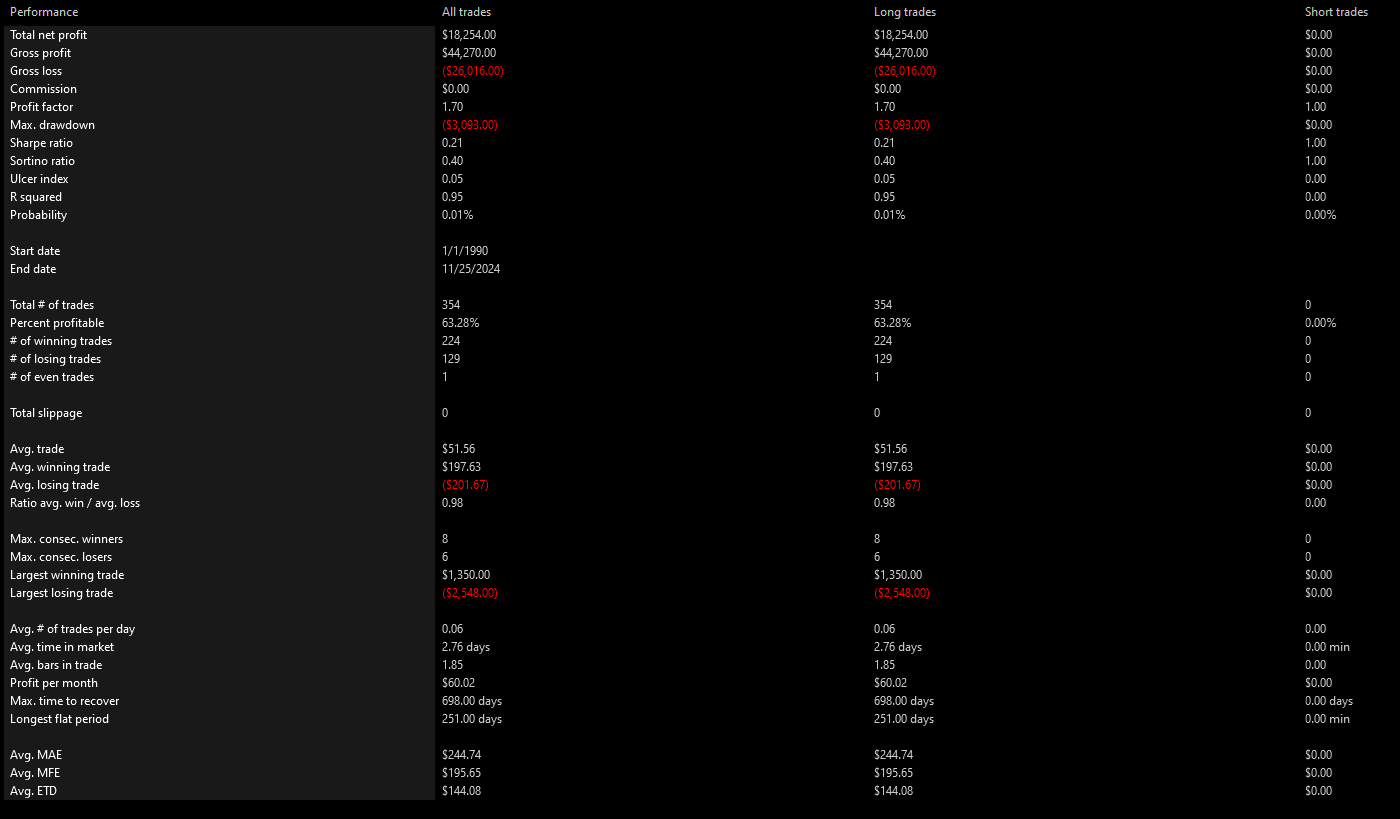

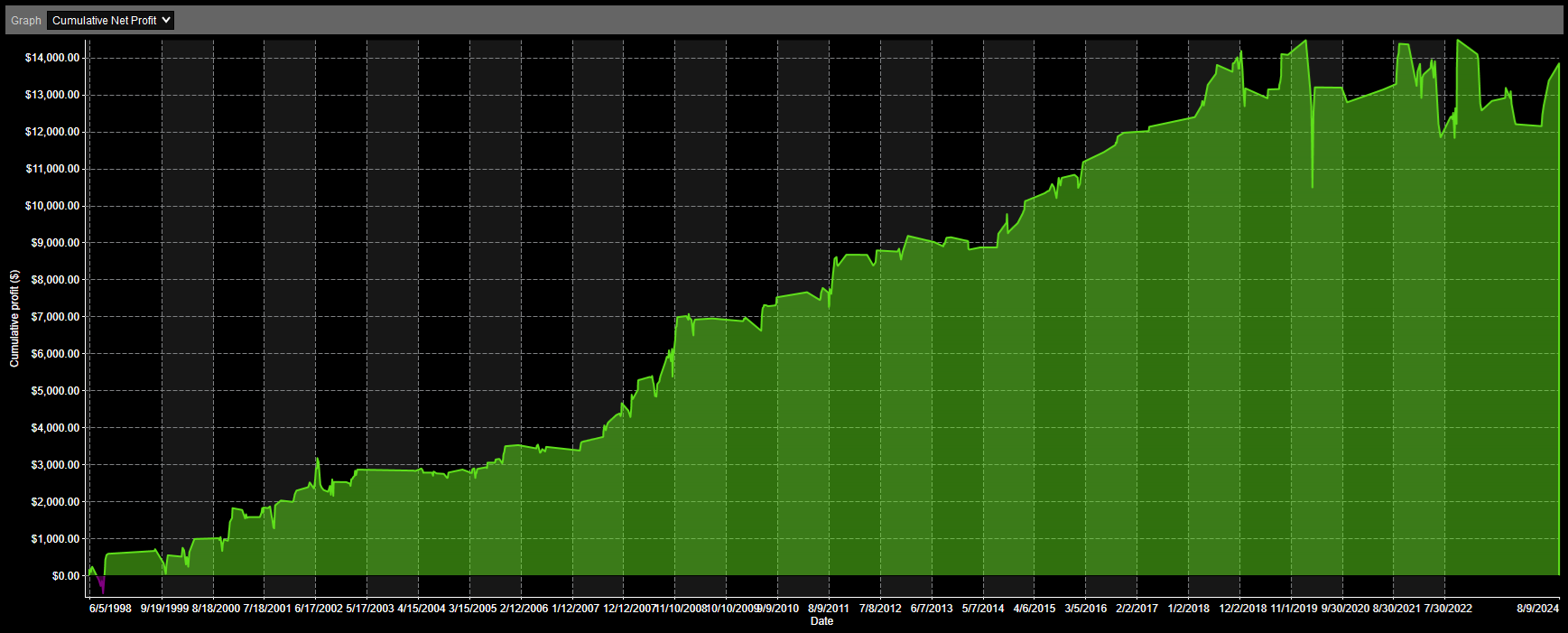

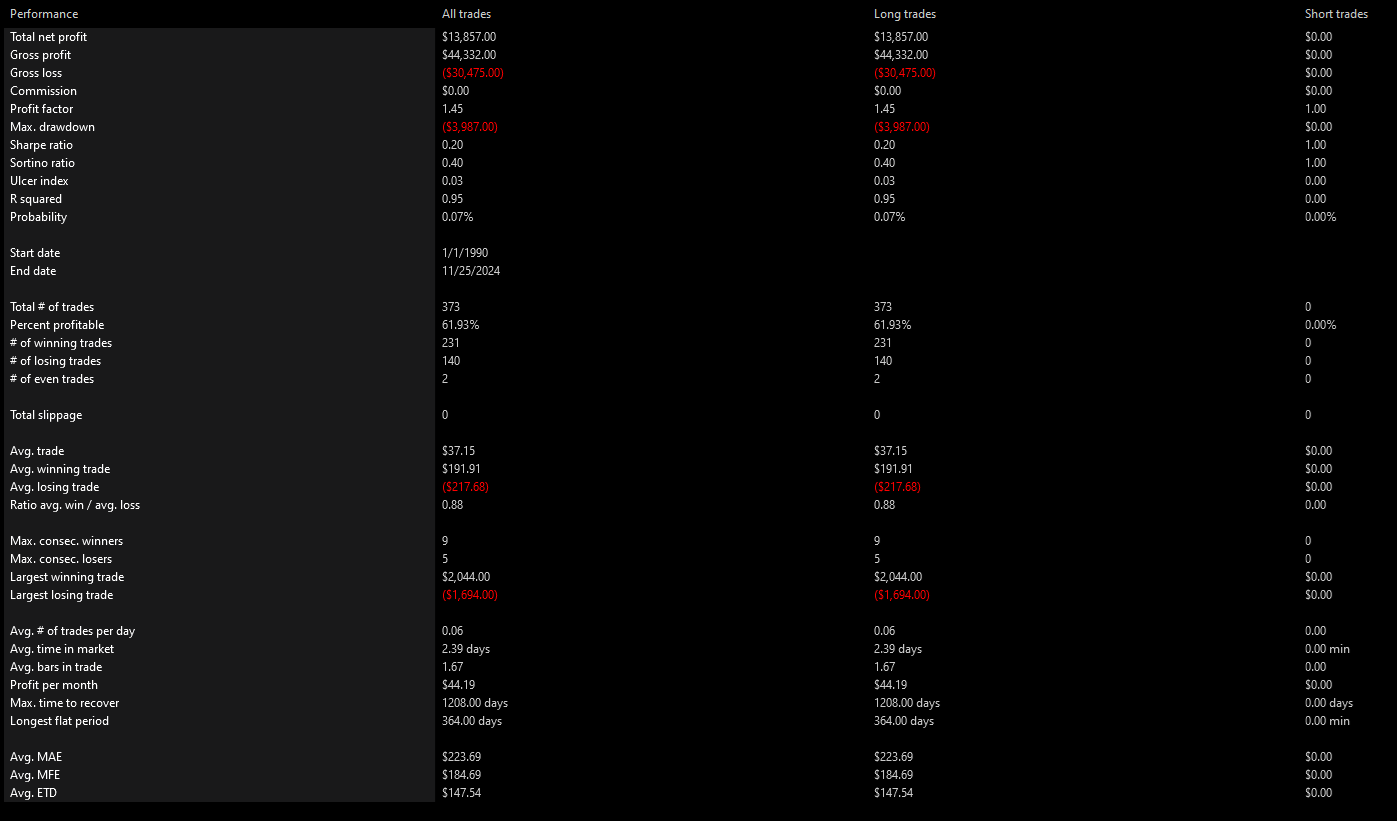

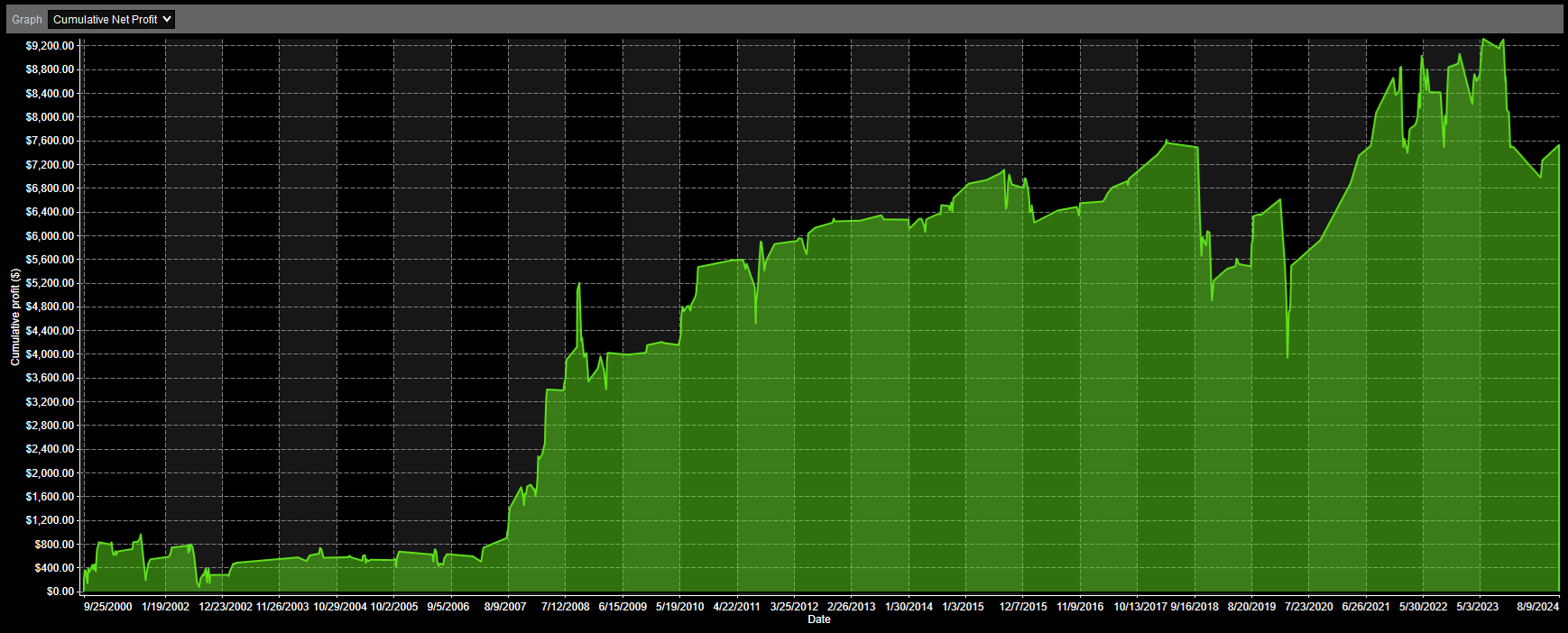

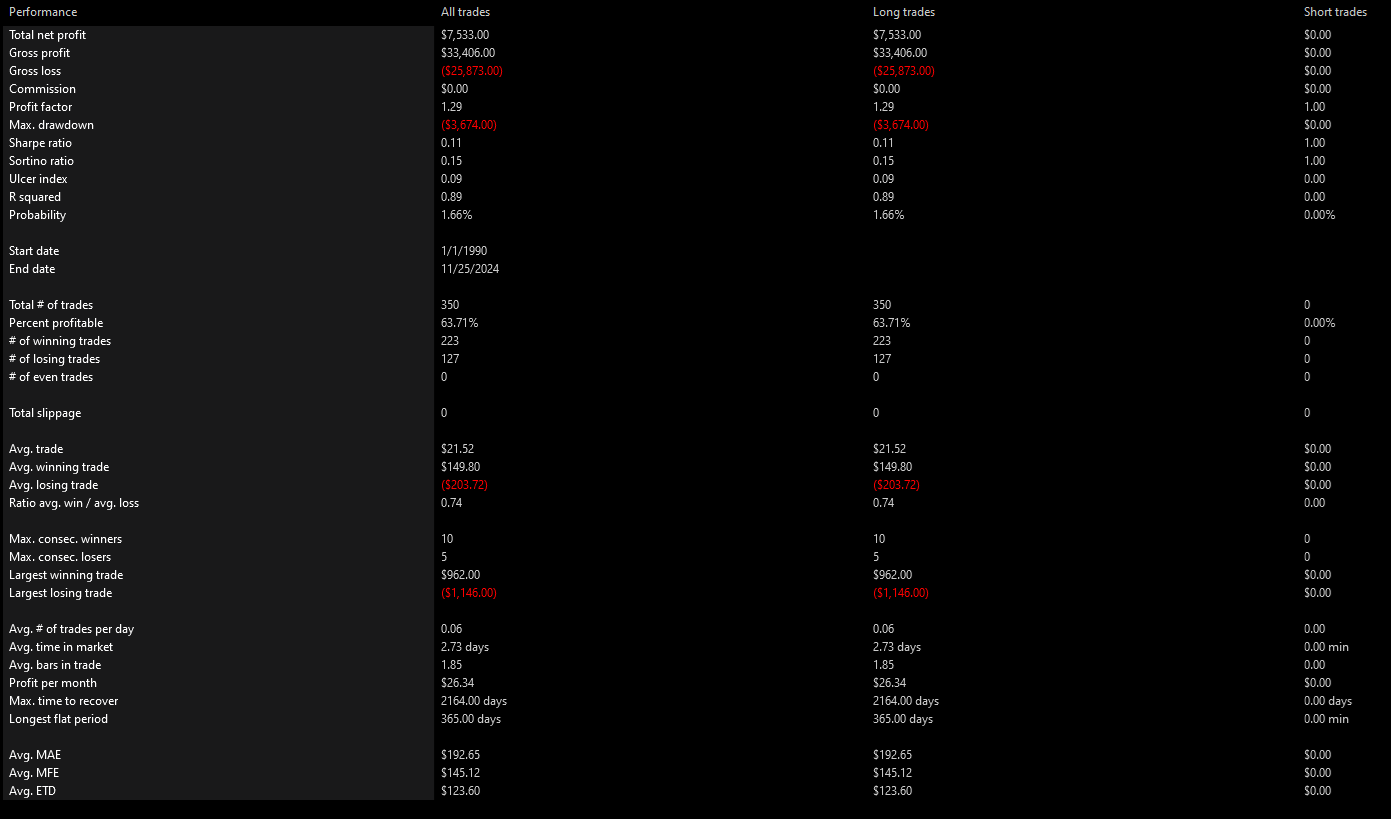

Backtest Results

SPY

QQQ

DIA

IWM

Sector ETFs

This backtest is an aggregation of the results of the following sector ETFs:

XLB, XLC, XLE, XLF, XLI, XLK, XLP, XLU, XLV, XLY